Top-line growth has returned but margins remain under pressure, according to LaingBuisson’s latest report on the central London private acute hospital market. Report author Ted Townsend drives down into the figures and asks how a sector which is soon to be home to three well-capitalised international medical groups will respond to the increased capacity and competition

Growth is back’ appears to be the headline for the private acute healthcare market in Central London, according to the latest research by LaingBuisson.

After a few years of low to negative growth, at least in the independent sector, the overall value of this market reached £1.59bn in 2018, a rise of 3.2% on 2017.

What is more, LaingBuisson forecasts that this will have grown by another 5.5% in 2019.

Recent growth continues to be driven by the private patient units (PPUs) of NHS hospitals, which now take up 25% of the market, an increase in share of c. 5% compared to ten years ago.

The PPUs continue to achieve annual revenue increases of c. 9% p.a., albeit these figures are dominated by the specialist hospitals of Great Ormond Street and the Royal Marsden.

But growth has also come back to the independent sector, with an increase of 1.6% in 2018 (compared to a decrease of 3.6% in 2017), and a further 4.3% increase expected for 2019.

Some hospitals, such as The London Clinic, are reported to have had over a year of consecutive month-on-month increases in revenue, and BUPA Cromwell is reported to have had its best month ever in late 2019.

Embassy patients return

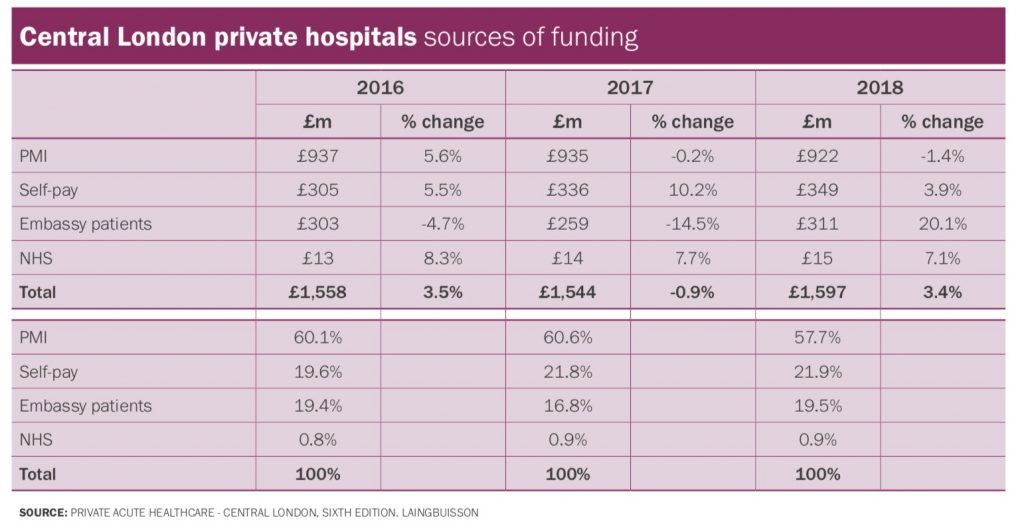

The main reason for the upturn is the return of embassy patients to the city, and in particular patients requiring more complex care.

Revenue from this source was up 20% across the market in 2018, compared to a fall of 14.5% in 2017.

There is some evidence to suggest patients are arriving ‘sicker’, as efforts to treat them in their home countries have not been as successful as hoped.

London has also benefited from a corruption scandal in the German embassy market, and a strengthened oil price.

There also appears to be greater willingness from London hospitals, particularly the independent ones, to invest in building relationships with organisations and individuals in the Gulf.

Such investment is bearing fruit in revenue terms, although there are still some questions about how sustainable it is in the longer-term because of costs.

Fall in PMI?

While private medical insurance still accounts for the greatest proportion of spend in the London market, 2018 saw a drop in this spend, at least in the independent sector, although this appears to have reversed in 2019.

Although insurers continues to pursue more standardised pathways offering better care but also better value for money and containment of costs, at the more complex end of care, such as oncology, this is harder to achieve.

LaingBuisson also reported continued growth in self-pay both for PPUs and independent hospitals. However, treatments purchased tend to be at the lower end in terms of pricing, and top-line revenue growth is still modest.

There remains a trend for people to ‘mix and match’ for more expensive procedures, for example by paying privately for a scan and then waiting for treatment on the NHS.

In addition, self-pay surgery tends to be lower-priced endoscopy or day-case procedures, and many of these procedures are needed to affect a top-line dominated by long-stay, complex care patients.

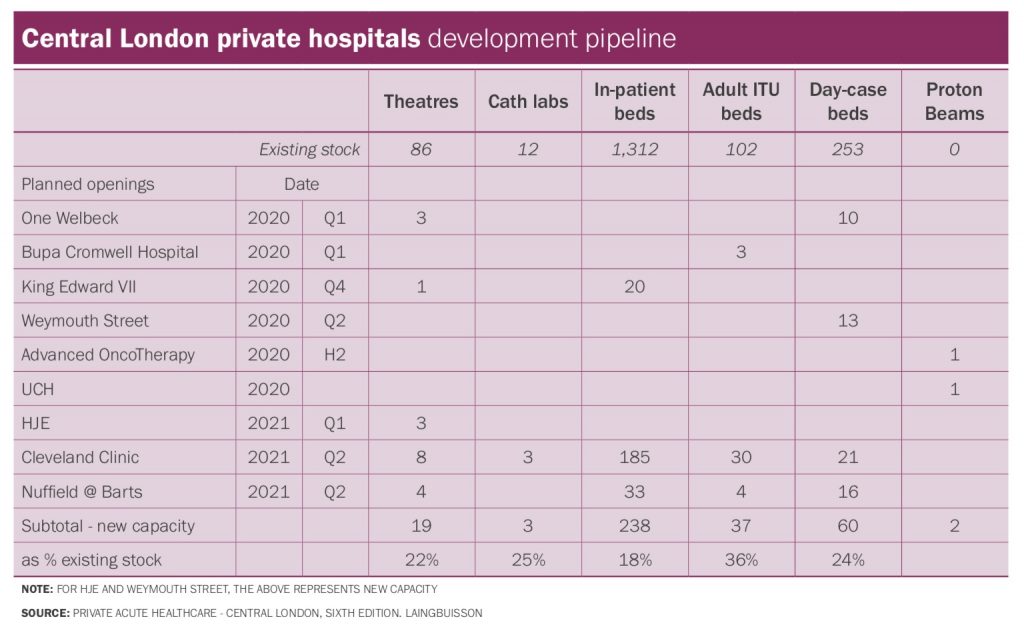

The report also discusses the changes to the market resulting from new entrants. Schoen Clinic and One Welbeck have both recently opened, with Schoen Clinic gaining an estimated 11% market share in orthopaedics within 16 months.

2020 will see further expansion of One Welbeck and the opening of new facilities at King Edward VII’s Hospital, and by 2021 expanded facilities at the Hospital of St John and St Elizabeth plus large new facilities such as Nuffield at Barts, and the Cleveland Clinic will have entered the market.

Margins under pressure

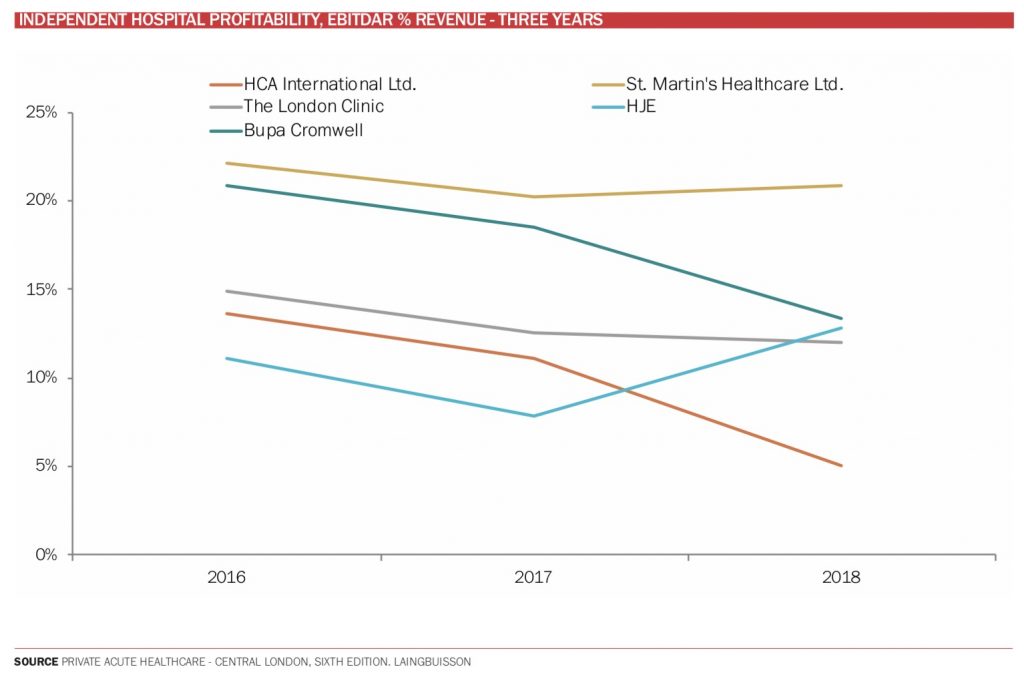

This increase in capacity will likely affect margins which are already under pressure.

Nearly half the EBITDAR available in the market in 2013 has now disappeared. The weighted average EBITDAR ratio as a percentage of sales has dropped from 22.3% in 2013 to 10% in 2018. Despite the recent increases in revenue, this does not appear to have helped the bottom line, as costs such as wages, governance and marketing all continue to go up.

Also going up are the costs of engaging with consultants. Whether this is through salaries and guaranteed bonuses or through other means such as splitting out portions of a hospital’s business and allowing consultants to co-invest, the different business models available from different, competing, hospitals suggest that the overall price of consultants will continue to go up, affecting hospital margins one way or the other.

In conclusion, this latest research points to some sort of industry consolidation or restructuring in the near future. Central London is now or will soon be home to three well-capitalised international medical groups in HCA, the Cleveland Clinic and Schoen.

Circle’s acquisition of BMI adds a new twist, as does Nuffield’s entry at Barts. The competitive picture looks very different than it did a few years ago.

One interesting possible development to watch is whether any hospital or group starts to treat NHS patients in any significant volumes. It may be the only way to generate the throughput to keep operations clinically safe as well as contribute to fixed overheads. Once one goes, others may follow.

{kind=link}